Good morning!

After firing Adam Neumann as CEO of WeWork, SoftBank offered to buy back over a billion dollars in employee stock, including $500M from the disgraced founder. Combined with the $185M in “consulting” fees that Neumann received to leave the company (i.e. to not consult), this was a pretty sweet severance package.

Well, according to new reports from the WSJ, Neumann recently managed to negotiate an additional $50M payout, a five year extension on a $430M loan that SoftBank previously made him, AND another $50M to pay for legal fees related to his exit.

This is the same guy that Vanity Fair called a Billion Dollar Loser. I get the sentiment, but… if you’re going to lose… do it like Adam Neumann?

It’s Saturday February 27, 2021.

Walking the Walk

In 2017, Zillow was sued by homeowners upset with their properties’ Zestimates, the company’s property value estimation tool. The suit accused Zillow of acting as an unlicensed appraiser and sought injunctions against the company’s publication of homes’ estimated values. The homeowners lost, appealed, and lost again.

On Thursday, Zillow doubled down and made its boldest Zestimate play to date, announcing the launch of a new cash offer product that will allow homeowners to sell their properties to Zillow with a single click, at the Zestimate price. Upon a homeowner’s election to sell, the company will send an inspector to verify the accuracy of the listing, pay all cash for the property, make some improvements, and then flip it.

The new program will begin in 20 markets covering 500,000 homeowners. Already the most popular real estate website (with its own SNL skit, no less), Zillow might now become the largest flipper in the country.

The new program’s success will largely depend on the Zestimates’ accuracy. In 2018, the median error for Zestimates (compared to sales price) was 6%, but 15% of the estimates were off by 20% or more. The accuracy has presumably improved since?

In any event, accurate or not, no one can accuse Zillow of not putting its money where its Zestimate is.

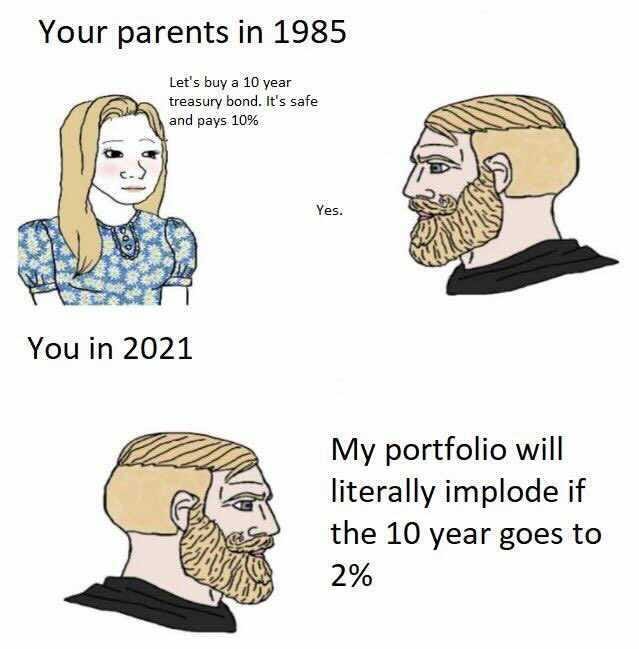

Yield Stuff

10-year treasury yields reached one year highs this week, wreaking havoc on equities and pretty much every other asset. I guess that’s bound to happen when stocks are priced to perfection with Year Infinity cash flows discounted at 0%?

Anyways, this hit close to home:

As a side note for email subscribers, memes feel like new age cartoons and Grant’s Interest Rate Observer famously publishes a cartoon per month; should The Saturday publish a meme per week? Reply to the email and let me know!

T+

People tend to like juicy stories, so it naturally follows that the Roaring Kitty vs. Ken Griffin narrative dominated the GameStop saga. Markets, however, are complicated and the real issues underpinning Robinhood’s January 26th decision to pull the plug on new GME purchases were more nuanced and technical than “hedge funds screwed the little guys, again.”

So, because not every story can have sex appeal, let’s talk about settlement periods.

As we previously discussed, volatility in GameStop stock led Robinhood’s clearinghouse, the Depository Trust & Clearing Corp., to demand an additional $3B in margin collateral. Robinhood likely didn’t have that cash on hand, so it halted buying instead. Where did that margin demand come from?

At a high level, clearinghouses receive transaction information from market participants, take positions opposite both the buyer and seller, and validate the transactions. It sounds simple, but there are a lot of transaction to be cleared. In 2020, for example, DTCC’s subsidiaries cleared and settled over $2.15Q in securities. Yes, Q as in Quadrillion.

When a trade is placed, and despite what your trading app may show, ownership of the security doesn’t actually transfer immediately. In the olden days, this settlement process for equities took 5 days. Today, trades settle two days after the transaction date. I.E. T+2.

The delay in settlement means buyers don’t need to have cash on hand at the time of transaction and that sellers don’t need to already own the securities. Both sides effectively have two days to get everything in order.

With longer settlement periods, however, comes greater counter-party risk, which in turn increases margin requirements. On average, any given day, DTCC’s clearing subsidiary holds $13.4B in margin (which also highlights the magnitude of Robinhood’s $3B margin call, when thought of as a percentage of average market-wide margin).

In the wake of the GameStop debacle, Robinhood and other observers have blamed T+2 settlement for outsized margin requirements and lobbied for a move to T+0 (aka real-time) settlement. Their prayers were (partially) heard.

On Wednesday, the DTCC published a white paper, announcing its intent to reduce settlement periods from T+2 to T+1 by 2023. While T+1 isn’t quite T+0, and 2023 is still two years away, this is a step in the right direction.

While it’s true that we already have technology to support T+0 - treasuries already settle on the same day - real time settlement creates a number of issues for parties trading equities on margin and others who cannot ascertain their financing needs until the end of the trading day.

More importantly, delayed settlement allows for the netting out of transactions, instead of money having to exchange hands for every single trade among common participants. In 2020, $1.77T in securities traded in an average day, but only $37.7B actually needed to change hands after netting out the underlying transactions. That’s a 98% decrease in payment volume, so fears that real-time settlement would overwhelm the system aren’t unfounded.

Moving the settlement period from T+2 to T+1 might not seem like much, but the expected benefits are substantial: according to DTCC estimates, margin requirements could drop by 41% in a T+1 environment. That’s nothing to scoff at!

With regards to changes being two years away, that’s suboptimal, I get it. WallStreetBets certainly wishes that the requirements had been lower in January. “GameStop would have gone to a $1,000,” they may say.

Still, considering the fact that it takes nine months for 50 Senators to agree on how to deploy $600 checks, two years to change the plumbing of a multi-quadrillion industry seems pretty reasonable!

OK, enough T+ talk for today.

Another One

In 2019, Morgan Stanley acquired Solium, a company that helped employees at startups like Stripe and Instacart manage their stock option grants. Last year, the bank acquired E*Trade for $13B, scooping up a competitor with an established footprint in the stock-plan management industry.

On Tuesday, Morgan Stanley continued its spree, taking over law firm Wilson Sonsini Goodrich & Rosati’s plan administration business.

WSGR is a renowned law firm based out of Palo Alto, California, with an impressive track record of advising successful (then-)startups, such as Google, LinkedIn, Lyft, Twitter, and many more. With stock option compensation being a staple of the startup world, WSGR developed software to help clients manage their employees’ holdings and, by all accounts, built up a substantial book of business.

With historically low interest rates and the advent of commission-free trading, banks and other financial institutions have been forced to reinvent themselves over the last few years. After Solium and E*Trade, acquiring WSGR’s plan administration business unit was a logical move for Morgan Stanley, who aims to be “the premier provider of financial solutions to workplace employees.”

Together, these acquisitions allow the bank to get a foot in the door with thousands of companies poised to mint future millionaires; millionaires who may later need wealth management advisory services or who may decide to sell their shares through the bank’s trading desk.

As always, nothing in The Saturday is investment advice and I have no meaningful basis to say whether Morgan Stanley overpaid for any of these deals, but this feels like a logical strategy. Now we’ll have to wait and see if it pays off.

Have a great weekend!